Prices for installed solar electric systems dropped again in 2015. Residential systems are 5% cheaper and commercial systems are 8% cheaper than the previous year. Tracking the Sun, an annual report published by Lawrence Berkeley National Laboratory, follows upfront cost before incentives. Prices for residential scale installations in the U.S. have dropped consistently from $12/Watt in 1998 to about $4/Watt in 2015 with some leveling off in the last few years. From 2008 to 2012, the main driver was a steep decline in photovoltaic (PV) module prices. Since 2012, module prices have remained relatively flat, while other components (inverters, mounting) and soft costs (labor, administration, marketing) have dropped faster. As system prices have declined, governments and utilities have deliberately reduced incentives, which now stand at less than $1/Watt in most areas.

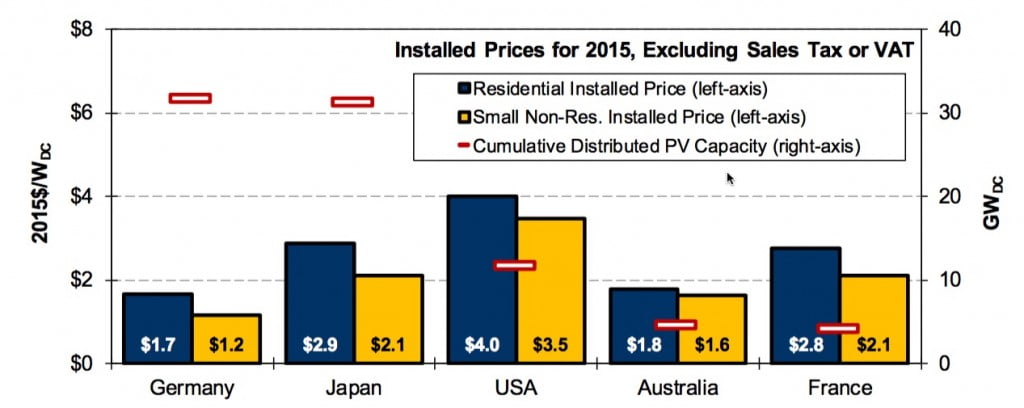

Of particular interest is the relationship of price in the U.S. compared to other countries. While hardware costs are similar across countries, the authors assign the higher costs in the U.S. and Japan to soft costs, which might include business models, interconnection standards, labor rates, and incentive levels, among others.

Not surprisingly, larger systems cost less per Watt. A typical 4,000 Watt system comes in around $4.50/Watt, while a 20,000 Watt system drops to $3.60/Watt. The report notes significant differences between states with Minnesota and New Mexico at the high end. Nevada and Texas cost the least. Most states are below the median price, but large numbers of installations in higher-cost states, such as California, New York and Massachusetts, push the national median higher.

While high-volume installers showed lower prices in Arizona, that wasn’t the case in other states where there was no apparent relationship between sales volume and price. Of particular interest to zero energy builders, installation prices were substantially lower in new construction than in retrofits. This may be due in part to the economy of scale in housing developments. Tax-exempt customers, such as schools, government, nonprofit and religious organizations, paid more than residential buyers, although the price has declined for all customers over the years.

The steady decline in the price of PVs, has supported the growth of zero energy buildings. Although module prices have probably reached their low, other hardware components still have room to drop. More importantly, soft costs still offer substantial opportunities. Incentives are likely to target these areas in the near future. Continued growth and evolution in the solar industry is good news for the zero energy movement.