Everyone agrees that many energy-saving improvements, such as adding insulation and high-efficiency heating systems, have benefits in the long run. These improvements benefit the contractors who install the improvements and the suppliers who provide the materials. Lenders make more money with lower risk because the borrowers have more stable monthly budgets. The money saved circulates multiple times through the local economy. And society benefits from reduced carbon emissions and reduced pollution. But few people take this opportunity because funding is often an obstacle and financial returns seem to come far down the road.

How can we encourage more people to undertake energy-efficiency projects and pay for them with sound financing? There is a simple market-based approach that encourages people of all income levels to finance and implement energy-saving home improvements. And it’s an approach that requires no subsidy.

The solution is simple. Most consumers and most lenders make financial decisions based on a sound monthly budget. To facilitate the approval of loans that do not add a burden to consumers, all we have to do is arrange financing so that the monthly savings from energy improvements exceed the additional monthly loan payment for the project.

Every home has a monthly utility bill. By reducing the utility bill, occupants gain buying power. Every $10 in savings is really $10 more income. So the income gained from energy-saving home improvements can be used to make the monthly loan payment. In essence, this means that energy-saving improvements can pay for themselves from the very first month.

For example, purchasing and installing a 50-gallon heat pump water heater might cost about $1500 and on average will save $330 a year on the energy bill for a household of four. The monthly savings will come to $28 per month, which will help the family qualify for a loan to install the equipment. For a 5-year, $1500 home improvement loan at 5% interest, the payment will come to $28 per month, so the savings will cover the loan payment. After five years, the loan is paid off and the energy savings keep coming each year after that.

It works the same way when you add up all the energy-saving upgrades used when renovating your home to zero energy or are purchasing a zero energy home. A simple mortgage calculation will tell you that $10 more income per month will allow a homebuyer to qualify for an additional $2000 in mortgage financing on a 30-year loan at 4% interest. (You can calculate this for yourself on any mortgage calculator. Just enter $2000 as the principal amount, 4% as the interest rate, and 30 years as the duration.) If, for example, energy modeling of your energy upgrades shows savings of $100 per month, which could be easily achieved, you will be creating $20,000 in borrowing power to finance the work.

For people who qualify for the loan based on their existing capital resources, this is a good investment, one that frequently beats stocks. For lower and middle income consumers however, there is often a missing link which, if fixed, would help many more people qualify for loans that cover the added costs needed for a zero energy home or energy efficiency upgrade to their current home.

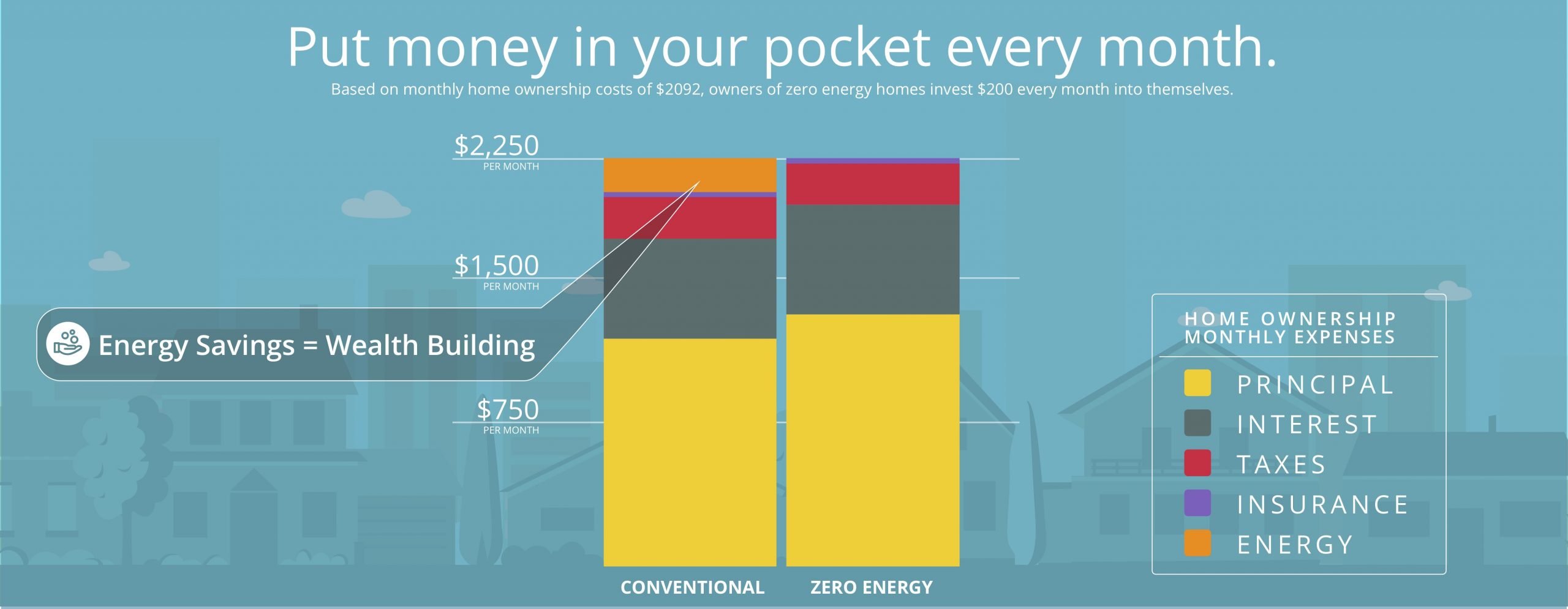

Lenders typically base a consumer’s loan approval in part on the cost of home ownership. They calculate a borrower’s expenses as principal, interest, taxes, and insurance – also called PITI. Energy costs are ignored even though energy bills are due every month and can be greater than some of the other factors that go into the lender’s calculation. If lenders would simply add energy costs to their calculation (PITI+E), a world of new opportunities would be available. In effect, occupants would be allowed to shift money from monthly utility bills (an expense) to home improvement, or a zero energy home purchase, financing (an investment). The total monthly budget would stay the same. Borrowers would be getting a better home for no additional cost, while the local economy gets a boost and emissions are reduced.

The chart below shows a comparison of the monthly payments for a zero energy home with the monthly payments for a similar code built home using typical numbers for PITI+E. While the payments in this example are equal, the owners end up with a much better home for the same cost per month. The energy savings from a zero energy home are actually added income that allows you to purchase a superior home. In other words, that is a smart investment!

Since current lending practices do not embrace this common-sense idea, legislation or new regulations may be required to compel mortgage lending regulators and the secondary mortgage market to include energy costs as a loan qualification criterion. This simple requirement will generate millions of dollars of business for local contractors and suppliers. Lenders will make more low-risk loans. Working people will have more stable finances and more comfortable homes. And as a society we will be further reducing our carbon emissions. This is a win-win-win solution.

Even though banks do not yet accept PITI+E as standard practice, there are lending programs that can be used by any lender, including Greenchoice from Freddie Mac and HomeStyle by Fannie Mae. With any loan product, documenting the value of home energy improvements and the modeled energy savings of the improvements is still important. Whether is a small energy savings project or a zero energy home, you can show these savings to the loan officer and/or appraiser as part of your documentation, and explain to him that these energy savings are really income that allow you to make the payments on the energy upgrades. Even though they do not officially make energy savings part of their formula, by documenting these earnings, you can build trust and confidence in your financial position and make it more likely they will approve the loan.

A Texas Builder Explains Total Cost of Ownership

“The old school of return on investment says you typically need to pay it back in about 6 years or so. With green building it’s a whole different story, and when I explain this to prospective clients they get it, whether they’re a wage earner buying an entry level home or an upper income person buying their second or third luxury move-up product. The return on investment on what you spend for green building is typically realized the first month you’re in the home.

Here’s a real example of a 3,000 square-foot home with a $300/month average utility bill. If you spend $10,000 additional on the green aspects of the home, you can reduce that energy cost to $150 per month. At today’s mortgage rates, the $10,000 you spend costs you about $30 per month. You’ve saved $150 in utility costs and you’ve spent $30 to do it. Your positive cash flow that first month is $120, and it will be at least $120 a month after that. Whenever I’ve explained that to a customer, whether they’re buying a $100,000 home or $3 million home, they’ve never failed to embrace it and find great value in it.”

–T.W. Bailey Sr., president of Bailey Family Builders, Frisco, Texas

One thought on “Financing Energy-Saving Improvements and Zero Energy Homes for All”